How a 2010 Colorado law suddenly stands to change internet sales tax collection for good

The Supreme Court declined to hear arguments challenging a law that requires ecommerce retailers to report consumer sales to the state.

The decades-long effort to give states the power to collect sales tax on purchases made online from out-of-state retailers took another turn this week when the Supreme Court declined to hear a case challenging a Colorado sales and use tax collection law. The decision not to hear the case opens up the potential for other states to follow Colorado’s creative lead in addressing tax collection on online sales.

The Colorado notify-and-report law requires that retailers without physical locations in the state notify residents about sales tax laws and send a year-end statement of purchases to residents. In addition, the law requires that retailers send a report to the state revenue service annually that includes customer names, addresses and purchase amounts annually. The law applies to retailers with at least $100,000 gross sales in the state and to residents who purchase at least $500 worth of goods or services with a retailer.

Currently, states require consumers to self-report use tax (sales tax paid by consumers) owed on purchases made from out-of-state retailers, but few actually do it. The Colorado law gives consumers a much clearer incentive to do so.

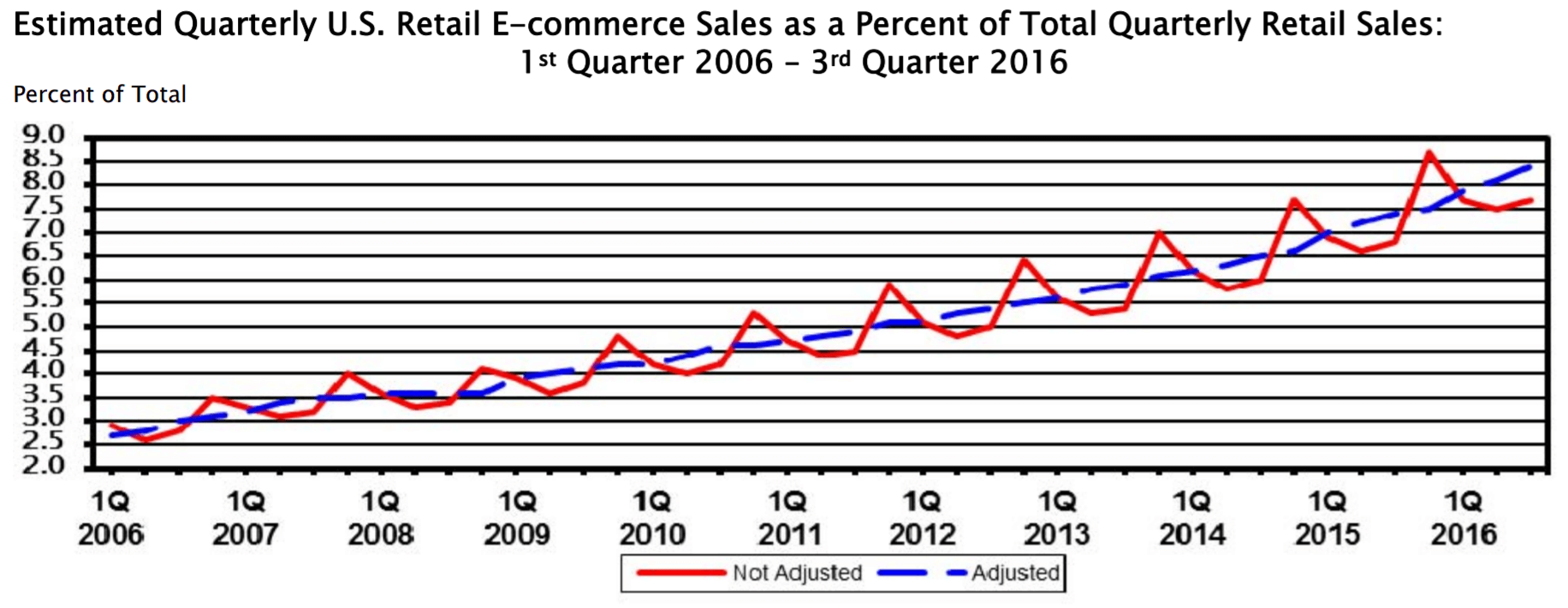

As ecommerce has grown as a percentage of overall sales, states have been looking for ways to collect taxes on all of those transactions. In the third quarter of 2016, ecommerce sales increased an estimated 15.6 percent year over year, according to the US Census Bureau, while overall retail sales increased just 2.3 percent. The bureau estimates US consumers spent $93.7 billion on ecommerce in Q3, or 8.4 percent of total sales on an adjusted basis. Colorado officials estimate the state misses out on as much as $172.7 million a year in tax revenue by not collecting from non-reporting retailers.

Source: US Census Bureau

How Colorado’s law sidesteps nexus requirements

In 1992, the Supreme Court set a precedent in the Quill case — which (fun fact) revolved around an office supply retailer shipping floppy disk orders out of state — that states may only collect sales tax from companies that have a physical location (or nexus) such as a store, warehouse or distribution center in that state. Some states have extended that meaning to include affiliates located in-state. Instead, consumers are supposed to tally up their purchases and file state use tax with their returns each year. That has proven to be a less-than-successful tax collection tactic.

Federal legislation that would require remote sellers with gross sales over $1 million to collect and remit sales tax in qualifying states has stalled for years.

Colorado’s creative workaround to require retailers to notify consumers of their tax responsibilities and report consumers’ purchases to the state gets around nexus laws because the state is not actually requiring the retailers themselves to collect and remit sales tax to the state. Opponents to the law have not gone quietly, however.

The winding path of a 2010 law through the courts

Shortly after the Colorado law passed, the New York-based industry group Data and Marketing Association (formerly the Direct Marketing Association), sued, putting the law on hold. The association argued the law put undue burden on out-of-state retailers. Direct Marketing Association v. Brohl (for Barbara Brohl, executive director of the Colorado Department Of Revenue), has since been on journey up and down and back up the court system for years.

This actually marks the second time this case has made it to the Supreme Court. In 2012, the 10th District Court ruled that Colorado’s notify-and-report law caused undue hardship for out-of-state retailers. But the Data and Marketing Association lost on appeal, not on the merits of the case, but because the 10th Circuit Court of Appeals ruled the District Court did not have jurisdiction over the case. The association then brought the case to the Supreme Court to determine if a state or federal court had jurisdiction. In March 2015, the Supreme Court ruled unanimously that the association could sue the state to have the law overturned.

The Supreme Court did not address the merits of the association’s legal challenge, however, it is worth noting that in his concurring opinion, Justice Kennedy called for reconsideration of Quill:

“The Internet has caused far-reaching systemic and structural changes in the economy, and, indeed, in many other societal dimensions. Although online businesses may not have a physical presence in some States, the Web has, in many ways, brought the average American closer to most major retailers. . . . Given these changes in technology and consumer sophistication, it is unwise to delay any longer a reconsideration of the Court’s holding in Quill. A case questionable even when decided, Quill now harms States to a degree far greater than could have been anticipated earlier. “

In February 2016, the 10th Circuit Court of Appeals upheld the law, finding “the Colorado law does not discriminate against nor does it unduly burden interstate commerce.” The Data and Marketing Association then appealed again to the Supreme Court, arguing the law entered the realm of interstate commerce, which is governed at the federal level. The Supreme Court’s refusal to hear that argument means the appellate court decision stands, opening the door for other states to initiate their own notice-and-reporting requirements for ecommerce retailers.

What’s next?

Whether online retailers are eventually charged with collecting and remitting sales tax or consumers are held more accountable for paying use tax on their online purchases, this case would appear to mark a turning point in the internet sales tax battle.

In response to the Supreme Court’s refusal to hear the case, Emmett O’Keefe, Data and Marketing Association vice president, told the Associated Press, “It will only encourage other states to adopt similar laws and regulations that are designed to put arbitrary burdens on out-of-state sellers.”

“This settles the issue, once and for all, that the 2010 law is constitutional, it was not an undue burden on business,” said Tim Hoover, spokesman for the Colorado Fiscal Institute, which supported the law.

Several states’ Attorneys General had filed a friend-of-the court brief encouraging the justices to hear arguments in Direct Marketing Association v. Brohl. On its face, the court’s decision not to hear it is good news for states looking to recoup taxes on internet sales. The Supreme Court could still take up the issue with another case, particularly if other states pass similar legislation.

Tennessee Governor Haslam’s proposed bill to require out-of-state retailers to charge sales tax just passed its first legislative hurdle on Thursday.

Incidentally, without advance explanation to the Colorado Department of Revenue, Amazon began charging sales tax in Colorado on February 1, 2016, making Colorado the 27th state in which the ecommerce giant charges consumers sales tax.

Contributing authors are invited to create content for MarTech and are chosen for their expertise and contribution to the search community. Our contributors work under the oversight of the editorial staff and contributions are checked for quality and relevance to our readers. MarTech is owned by Semrush. Contributor was not asked to make any direct or indirect mentions of Semrush. The opinions they express are their own.

Related stories

About the author