Google Q3: Earnings, Revenues Miss, Paid Clicks Up, CPCs Down 2 Pct.

Google announced Q3 2014 earnings this afternoon. The company reported $16.52 billion in “consolidated revenues.” This represented a 20 percent increase over Q3 2013. However earnings per share and revenues were below Wall Street expectations. The stock is off in after-hours trading. Google sites generated $11.25 billion, which was 68 percent of total revenue (20 percent […]

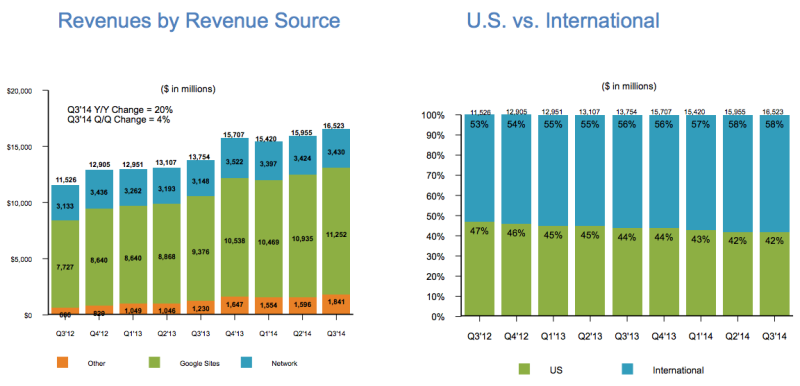

Google announced Q3 2014 earnings this afternoon. The company reported $16.52 billion in “consolidated revenues.” This represented a 20 percent increase over Q3 2013. However earnings per share and revenues were below Wall Street expectations.

The stock is off in after-hours trading.

Google sites generated $11.25 billion, which was 68 percent of total revenue (20 percent increase year over year ). Network/partner site revenues were $3.43 billion, which was a 9 percent increase year over year. Other revenues (Google Play primarily) were $1.84 billion, a 50 percent increase vs last year.

Revenue from outside the US was $9.55 billion (58 percent of total revenue). UK revenue in particular was $1.63 billion.

Traffic acquisition costs were $3.35 billion, up from $2.97 billion in 2013. CPCs were down 2 percent year over year but constant from Q2 2014. CPCs on Google and and its network both declined:

Cost-per-click for Google sites decreased approximately 4% over the third quarter of 2013 and decreased approximately 1% over the second quarter of 2014. Network cost-per-click decreased approximately 4% over the third quarter of 2013 and increased approximately 2% over the second quarter of 2014.

Paid clicks increased 17 percent vs. 2013 and grew 2 percent compared with the second quarter:

Aggregate paid clicks, which include clicks related to ads served on Google sites and the sites of our Network members, increased approximately 17% over the third quarter of 2013 and increased approximately 2% over the second quarter of 2014. Sites paid clicks, which include clicks related to ads we serve on Google owned and operated properties across different geographies and form factors including search, YouTube engagement ads like TrueView, and other owned and operated properties like Maps and Finance, increased approximately 24% over the third quarter of 2013 and increased approximately 4% over the second quarter of 2014. Network paid clicks, which include clicks related to ads served on non-Google properties participating in our AdSense for Search, AdSense for Content, and AdMob businesses, increased approximately 2% over the third quarter of 2013 and decreased approximately 4% over the second quarter of 2014.

Google said that it had roughly $62 billion in cash and cash equivalents, up from $59 billion at the end of last year. The company employed 55,030 full-time employees (including Motorola Mobility) as of September 30.

The earnings call is next and we’ll be listening for more color especially about the CPC decline.

Notes and comments from the earnings call:

On the call were CFO Patrick Pichette and Chief Business Officer Omid Kordestani. CEO Larry Page, because of issues with his voice, hasn’t been on the last few conference calls.

Pichette:

- “Aggregate CPCs were down only 2 percent.” Emphasis on the word “only”

- US revenue up 15 percent.

- Non-US revenue (not incl. UK) was up 26 percent

- Omid Kordestani returns to full time work and promoted to “Chief Business Officer”

Kordestani:

- Launched cross-device measurement for mobile display under Enhanced Campaigns. This has revealed 15 percent better conversion rates than previously recognized.

- The core of our business, performance advertising, continues to deliver great results.

- In our brand business . . . We’ve sold out our Google YouTube preferred ad inventory

- New brand ad formats for mobile devices launched

- DoubleClick bid manager is the “go to” tool to help marketers navigate the programmatic universe

- Remarkable momentum in our new non-ads business. Google Play’s growth “continues to impress.” Play movies available in 93 countries.

- AndroidOne will be expanding to India, Indonesia in the coming months.

- 250 million active Google Drive users

Financial analyst Q&A:

UBS asks about Google Shopping Express, its rebranding (Google Express) and any momentum.

Kordestani: “Our goal is to take it a step at a time.” Pichette (defensively): it’s very clear that people want this product. Now we’re in phase 2 according to our business plan. You should see the announcements this week as a good sign.

Merrill Lynch asks about paid clicks and CPCs:

Pichette: We’re happy with monetization, which is very strong. There’s nothing noteworthy to mention this quarter, “we’re very happy with the trends.”

Credit Suisse asks about where Google is investing in its business:

Pichette: We’re investing in our core business. But investing in many other areas “with enthusiasm.”

RBC Capital Markets asks about mobile search health/usage:

Pichette: Mobile is still a big part of our growth. CPCs can fluctuate from quarter to quarter. We’re very pleased with the momentum.

Question about UK market and its health and mobile payments:

- Pichette: UK slowing growth a result of multiple factors. But we’re happy with it.

- Kordestani: We’re developing a fully functional payment system. Cites a range of consumer features. But focus is on merchant adoption.

Question about TV budgets and shift to online:

Kordestani: we are seeing a shift to digital with brand advertising. Re Facebook . . . what they’re doing is bringing more attention and innovation to the space so we welcome that. There 400 hours of content uploaded every minute.

Question about deep linking and mobile apps:

Kordestani: AdMob reaches 900 million unique devices every month. Our own apps are very successful. We’re helping to drive hundreds of millions of app downloads for developers. We’re focused on this area to help developers.

Pichette: we see significant developer adoption of deep linking

Question about mobile ad pricing:

Pichette: on a QoQ basis don’t panic about CPC fluctuations

Question about estimated total conversions and movement away from cookies:

Kordestani: it’s going to take awhile to have a real end-to-end solution for marketers and partners. References audience targeting on Facebook. No response regarding cookie replacement with ID alternative

Follow up question about Google Express and digital wallets (does Google need to own the Android payment solution?)

Pichette: With Google Shopping Express there is an issue of scale. Trials off into generic discussion of efficiency

Kordestani re payments: we want to get the user experience and the ecosystem right

Question about how the carriers are reacting to Google Play:

Pichette: we have good relationships with carriers

Question about Google video advertising:

Kordestani: we have upfront (YouTube) commitments for Google Preferred from five top agencies and major brands. We’ll continue to figure out how to package this inventory better and working with advertisers and agencies to get “this time of selling right.”

I didn’t capture every question or response but got most of them. Largely Pichette and Kordestani responded in unspecific generalities that were quite bland. Things are going well for Google but clearly not as well as portrayed (they missed on earnings and revs). Even while maintaining their upbeat tone and outlook they could have more directly answered a number of the questions and provided more detail than they did.

Contributing authors are invited to create content for MarTech and are chosen for their expertise and contribution to the search community. Our contributors work under the oversight of the editorial staff and contributions are checked for quality and relevance to our readers. MarTech is owned by Semrush. Contributor was not asked to make any direct or indirect mentions of Semrush. The opinions they express are their own.

Related stories

About the author